PA Manufactured Housing Association

Manufactured Housing Authority

FAQ's

Find questions and answers to the most commonly asked questions regarding factory-built homes.

Why Buy Factory-Built?

Want to see what living in a manufactured home can be like? PMHA has provided a video to showcase the industry and give insight into how these homes are built.

Find a Home

Our member retailers are experienced in assisting consumers with finding the perfect factory-built home.

Membership

As a member of PMHA, you will quickly see that our primary goal is to be your one-stop resource center. We offer our members many networking / educational opportunities, advocacy through an active PAC, numerous resources and services, marketing opportunities and unique member only savings.

Click here for more information

Not a member? Learn how to join.

Become a MemberMember Benefits:

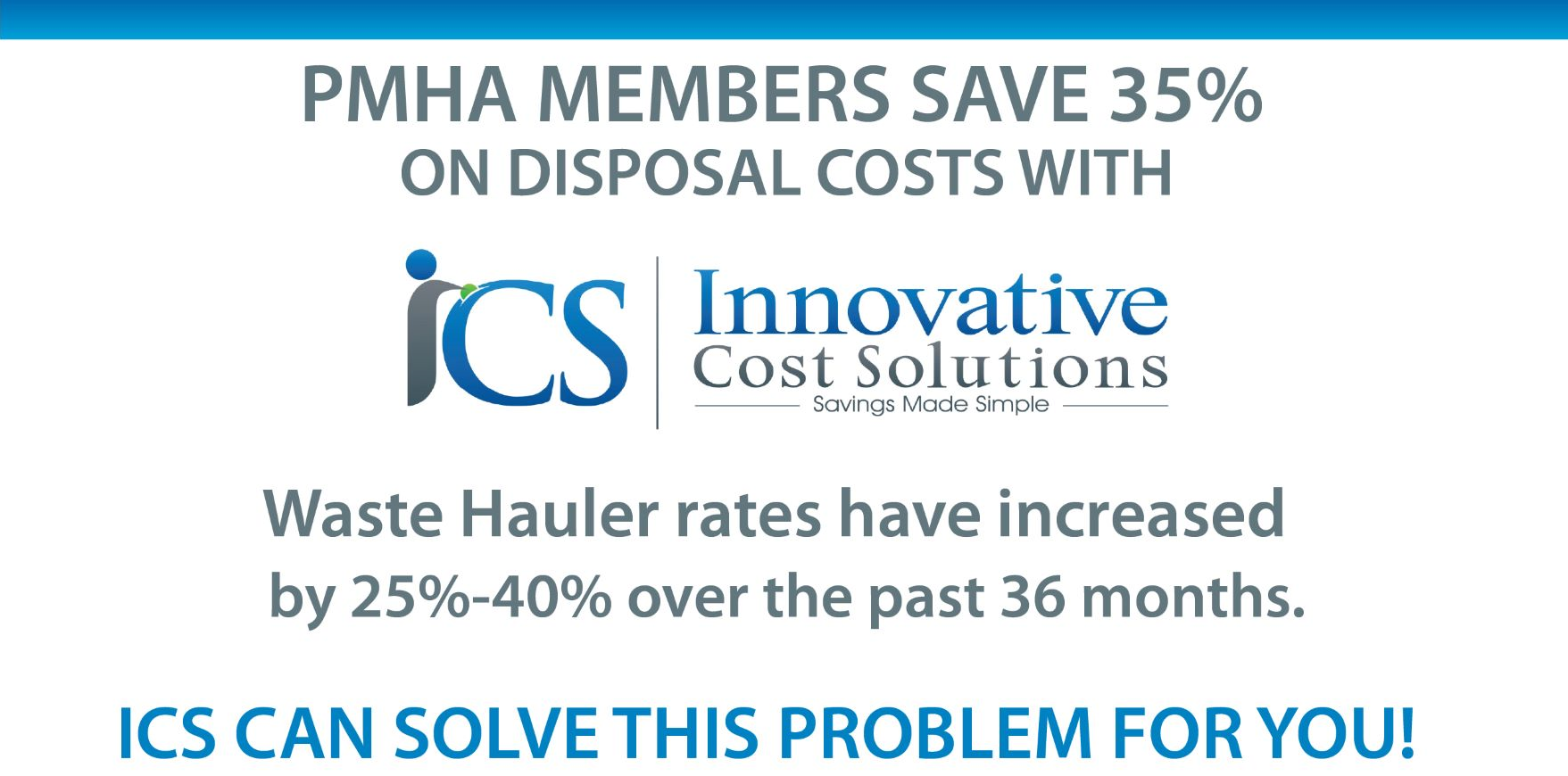

APPI Energy is available to provide data-driven, holistic energy management services and custom solutions to PMHA members at no upfront cost or obligation to you. As part of your membership benefit, APPI Energy can analyze your energy usage, evaluate your energy bill, deliver a green-apples-to-green-apples comparison of supplier prices and contracts, and negotiate a supply solution tailored to your budgetary needs and sustainability goals. In addition to electricity and natural gas procurement strategies to help you secure more favorable pricing and contracts, APPI Energy offers energy management solutions to reduce demand, reduce costs, and increase sustainability. For more information, contact their team today at 800.520.6685 or info@appienergy.com. Read More!

Click here for APPI's FAQ

Industry Happenings

Industry Resources

MHI’s Government Relations staff has developed a new advocacy website to make contacting Congress about issues facing the MH industry easy. Read More...

PMHA offers many Industry Resources see what we have to offer - click here

Most current version of Act 261 - Act 261 governs Manufactured Housing Communities and provides details of recent amendments and new requirements. Continue Reading...

Corporate Partner

Advertisers

![]()

Pennsylvania Manufactured Housing Association serving and promoting the Factory-Built Housing Industry.